In this piece, Anthony Pygram, Senior Manager within our Strategy, Analysis and Monitoring division talks about our work on card fees.

We’re looking at the fees card schemes charge for card transactions – and whether we need to act over recent rises. We announced this work in November last year. Since then, we’ve been gathering and analysing information to help us identify where we should direct our attention. Later this month, we’ll consult on draft terms of reference for two market reviews of card fees. These documents will set out the purpose and proposed scope of the market reviews. We’d like anyone with an interest to give us their feedback and help us shape our work.

Cards are the most common payment method in the UK, which makes them critical to the smooth running of the economy. In 2021, people made 21 billion payments on UK-issued debit cards, totalling £702 billion. UK-issued credit card payments numbered 3.5 billion and amounted to £182 billion. As the UK’s regulator of payment systems, we want to make sure that payment systems work well for people and businesses.

We’re focusing on two categories of fees associated with card payments. These fees are ultimately paid by merchants when they accept card transactions:

-

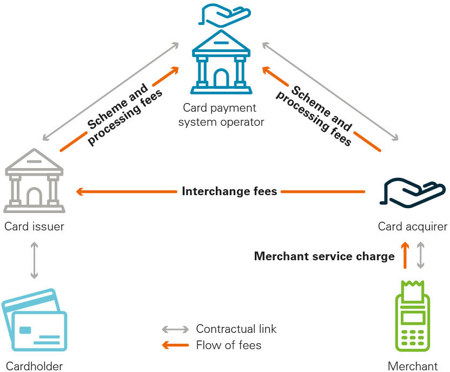

Scheme and processing fees: Card payment system operators charge card issuers and acquirers for using the system, and processing entities charge them for each transaction. Card issuers are institutions like banks issuing customers with debit or credit cards. Card acquirers provide the services that allow merchants to accept card payments.

-

Cross-border interchange fees: In a four-party card payment model used, for example, by Visa and Mastercard, the acquirer pays an interchange fee to the issuer for each transaction. When someone makes a card payment, their card issuer takes the money from their account and passes it on to the acquirer – minus the interchange fee. We’re prioritising interchange fees paid on transactions using cards issued by EEA banks to buy from UK merchants, also referred to as “outbound” interchange fees.

In our card-acquiring market review, we found that scheme and processing fees paid by acquirers had increased significantly from 2014 to 2018 – and merchants have told us that scheme fees have continued to increase. Our new work builds on these findings. We’re also considering scheme and processing fees that issuers pay to operators, to understand the overall flows of money.

Cross-border interchange fees have also increased significantly in the last year. In particular, this affects fees for certain card transactions between the UK and the EEA, where the cardholder is not present (such as payments made by phone or online). Since the UK left the EU, Visa and Mastercard have increased these fees fivefold.

We’ve decided to continue our investigations into these concerns by carrying out two market reviews. One will look at scheme and processing fees, and one at cross-border interchange fees. Market reviews are one of our tools for investigating how well the markets for payment systems work for service users. In this case, we want to know the impact of card fee increases on UK merchants and consumers. The fact that the two main card system operators can increase these fees could indicate that the market is not working well.

The market reviews support the PSR Strategy, which sets out our priority to ‘promote competition between UK payment systems and the markets supported by them, protecting users where that competition is not sufficient’. In the long term we want to unlock the potential of different ways to make payments, such as account-to-account payments. In the meantime, we want to address any harm that may arise from scheme and processing fees and cross-border interchange fees.

We’ll publish the draft terms of reference in June, setting out our proposed scope of work and the areas we’ll explore. The consultation will run until the end of July. We’re planning a number of engagement events with stakeholders during the consultation. We’d like everyone with an interest to provide their feedback and help us shape our work.

If you have any questions or concerns, or would like to tell us how changes in scheme fees or cross-border interchange fees have affected you as a merchant, consumer or provider of payment services, please contact the project team at [email protected].