What we’ve seen so far – our assessment

The data shows positive outcomes for consumers in the first year of our policy. Reimbursement rates were high, firms responded to claims promptly, and there was no indication of people being significantly less cautious. Over the past 12 months, we’ve seen claim volumes fluctuate as the reimbursement requirement took time to bed in.

In the first year (between 7 October 2024 to 30 September 2025):

-

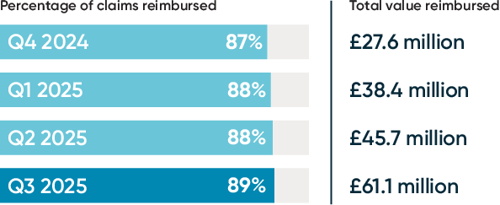

88% (£173m) of the money lost to APP scams has been reimbursed to victims. For comparison, UK Finance reported a 65% reimbursement rate in 2024.

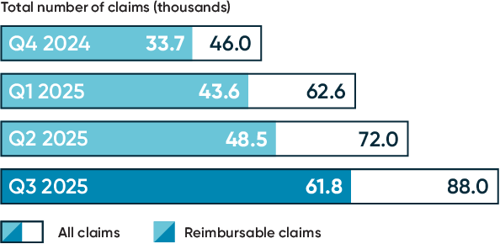

- Consumers have reported around 269,000 claims; 188,000 were in scope for reimbursement. This is around 15% fewer claims than the previous year.

-

82% of claims were closed within five business days – and 98% within 35 business days.

-

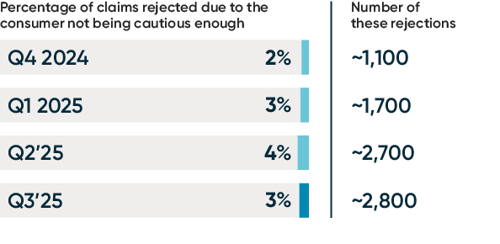

3% of claims rejected due to the customer not taking enough care over the transaction or their claim.

Introduction

This page shows data on authorised push payment (APP) scams and how payment firms reimburse victims.

The data helps us to monitor the impact of our APP Scams Reimbursement Requirement.

View our APP scams reimbursement data charts

The data

The data used in this dashboard is the latest available data covering 7 October 2024 to 30 September 2025.

It includes closed APP scam claims from payments made in the UK over Faster Payments within the reporting period.

There are notes on the data at the end of the page and under each graph. From time to time, figures may be updated as part of checking and verification of data. We will ensure any changes are clearly signposted.

Reimbursement

This chart shows the percentage of money lost to reimbursable APP scams and is returned to victims. It also shows the amount reimbursed per quarter.

-

Q3 2025 reimbursement rates for claims in scope of the policy remain high, increasing slightly by 1% from Q2 2025.

-

While we can’t make direct comparisons, we note that UK Finance reported a 65% reimbursement rate on personal accounts in 2024.

Consistency of outcomes

This chart shows the proportion of total claims that firms closed within five business days. This includes claims that they reimbursed, and claims rejected because they didn’t meet the definitions of the policy.

-

The proportion of claims resolved in five days dropped to 78% in Q3 2025, but the overall total since October 2024 remains strong.

APP scams claims

This chart shows the volume of claims made by consumers, and the proportion that were reimbursable under our policy.*

-

Q3 (1July to 30 September) saw around 62,000 reimbursable claims.

*There are various reasons why an APP scam claim is not reimbursable under the policy, for example if it is a civil dispute. The list of rejection reasons is in our Compliance Data Reporting Standards.

Consumer caution

This chart shows the percentage and number of claims that were rejected due to the consumer not being cautious enough (also known as claims that have not met the consumer standard of caution).

-

The number of claims rejected due to insufficient consumer caution remains low, with 3% rejected in Q3 2025.

Scope of the data

- An APP scam is when a consumer is deceived into sending a payment. For example:

- the person receiving the funds may not be who they say they are, or

- the funds may not be used for the purposes which the victim transferred the funds for.

- The data considers Faster Payments (FPS) APP scams where the reported victim is a consumer. As per our Specific Direction 20 (SD20), this includes individuals, small businesses or charities with an annual income of less than £1 million.

- The data used in this Dashboard has been shared with us by Pay.UK, the operator of FPS. Our SD20 requires directed payment firms to collect, retain and provide data and information to Pay.UK so that it can monitor compliance with the FPS reimbursement rules. This Dashboard uses the data provided by sending firms as per reporting standard A in the Compliance Data Reporting Standard (CDRS).

- All claims included in the data occurred on the Faster Payments system, within the UK. We note that some public reporting of, and research into, APP fraud is broader than faster payments – e.g. in relation to crypto scams.

- The data only includes APP scam claims that were reported to firms and were closed within the reporting period specified in ‘The Data’ section of the Dashboard.

- A closed APP scam case means the payment firm has completed an investigation of the case and made a decision on whether to reimburse the customer or reject the claim for one of the specified reasons. These rejection reasons are set out in Metric 2.3 in Compliance Data Reporting Standard.

- The data does not include ‘on us’ APP scam reimbursement. This is where both the sending and receiving accounts are within the same firm, and the transactions pass via an internal book transfer.

- The data accuracy and completeness are subject to the information provided by sending firms. We do not have information from receiving firms to validate the information.

- We continue to review and refine the data we receive. We may revise data for various reasons such as errors in compliance reporting or wrongly assigned claims. We may update figures as appropriate and will list any changes in these notes.

Revised data

-

- Please note that since the ‘Snapshot’ blog was published (with data covering the first three months of the Reimbursement policy), we have received revised data for December 2024 from Pay.UK. This dashboard uses the revised data set and therefore figures differ slightly from the blog, namely, the reimbursement rate which we reported in the blog as 86%, this has now been revised up to 87%.

Chart details

Chart 1 Reimbursement

Explanation

- Calculating the reimbursement rate: we have measured reimbursement as the amount of money returned to victims of APP scams where the claim is reimbursable. Calculation: CDRS Metric 7.1.2 (Total value reimbursed to the consumer) divided by CDRS metric 2.1.2 (total value of FPS APP scam claims that are reimbursable).

- Metric 2.1.2 includes the value of APP scam below the £100 excess, above the maximum cap (£85,000) and transactions within a claim that are rejected for reimbursement (‘non reimbursable’ due to one of the reasons listed at paragraph 6) when there is one or more transactions with the claim that are reimbursable. We are unable at this time to exclude the ‘non-reimbursable’ value from 2.1.2, which could increase actual reimbursement rates. In addition, metric 7.1.2 includes any value reimbursed above the maximum level of reimbursement. We have chosen to calculate reimbursement this way as we believe it provides the most accurate reflection of the money being returned to APP scam victims as per the reimbursement rules.

- Comparisons are indicative and the differences in the data sets must be considered. The data used for 2024 is from UK Finance’s Annual Fraud Report 2025 p.33. We have calculated this percentage using value data for ‘personal’ payments/cases only as we believe this to be more comparable to the consumer in SD20. Differences between the data include: the introduction of the reimbursement policy, a significant change in the definition of APP scams, calculation methods (e.g. for reimbursement rates), the number of firms in the data set. When calculating our reimbursement rate and claim numbers, we have not considered claims that have been rejected for the reasons listed in paragraph 6, as they are out of scope of the policy. However, UK Finance’s data looks at cases and likely uses a different definition of an APP scam so the same claims may not be excluded, making the value of total claims hard to compare. As an example, claims involving international payments or non-FPS payments may be included in UK Finance calculations but not in the PSR’s. The comparison also does not take into account the seasonal variation of APP scams.

Chart 3 APP scams claims

Explanation

- This figure includes ‘total claims’ as per metric 1.1 of the compliance data reporting standard (CDRS). It includes all claims that are submitted by a consumer as an FPS APP scam within the reporting timeframe even if it’s later determined by the firm not to be in scope of reimbursement. It also includes ‘reimbursable claims’ as per CDRS metric 2.1.2 of the CDRS.