Latest figures from the PSR dashboard show that in the first nine months following the introduction of the reimbursement policy:

- £112 million was reimbursed to victims

- 97% of claims were resolved in 35 days and 84% of claims were resolved within five business days

- Claim volumes are down – this shows that firms are stepping up and stopping fraud in response to the requirements

Marking the first anniversary of the Authorised Push Payment (APP) reimbursement requirement (7 October), the Payment Systems Regulator (PSR) shares its latest reimbursement data and key findings from its APP fraud survey.

A year of greater protection

In the year since its reimbursement requirement came into effect, the PSR’s APP scams policy has helped protect victims of APP fraud and incentivised firms to prioritise fraud prevention.

Data from the PSR’s quarterly reimbursement dashboard indicates consistent, positive outcomes for consumers:

- Reimbursement rates for APP scams are high: 88% of the money lost to APP scams and claimed back from a payment firm was returned to victims. This has significantly increased from 66% for the same period in 2023/24.

- Increased response times to claims: Firms resolve a significant majority of claims (84%) within five days and resolve nearly all (97%) within 35 days.

- Claim volumes are down: 126,000 claims were made between October 2024 and June 2025, around 15% lower than between October 2023 and June 2024. This shows the policy is having a positive impact as firms have stepped up and are spotting and preventing fraudulent transactions from happening in the first place.

David Geale, Managing Director at the PSR, says:

“Reaching the first anniversary of the reimbursement policy is a huge milestone. We have seen strong, positive early outcomes with payment firms stepping up by preventing fraud from happening in the first place and reimbursing victims quickly. This simply wasn’t happening consistently before our policy came into force.”

The PSR focus remains on ensuring victims are treated fairly, firms maintain high standards of compliance, and trust in digital payments continues to grow. In spite of the positive impacts the policy has had so far, the PSR has always been clear it would also make sure an independent evaluation would be carried out. This evaluation is now underway and the PSR will consider whether any aspects of the policy should be reviewed when that report is delivered in the spring.

David Geale continued:

“Bringing in significant reforms like these is a big change, and we are conscious that there may be things that could be done differently. That’s why this evaluation is important – so we can assess what has worked and where things might be done differently.”

Exploring the impact APP fraud has on victims

In addition to the latest dashboard, the PSR has also released its findings from its APP fraud survey of consumers. These findings show:

- Experiencing fraud has a limited or positive impact on trust in most organisations, except social media where trust tends to be lost: Of those who experienced fraud, 42% said their trust in their bank increased, whereas 38% of victims trusted social media platforms less.

- Reimbursement continues to have a positive impact on victims’ levels of trust: Half of victims who were reimbursed report trusting their bank more compared to around 1 in 3 of those who were not reimbursed.

- Purchase fraud continues to be a problem: Of those who fell victim to APP fraud, almost 60% fell victim through purchase frauds. The findings also show increases in delivery fraud, impersonation fraud and charity fraud.

- There remains low awareness of the reimbursement policy: For the first time, the PSR specifically sought to understand whether people knew about the policy. 49% of victims of fraud did not attempt to access reimbursement and 71% say they are unaware of the policy. In other consumer research published by the PSR earlier this year, the majority of people felt reassured that a protection like this exists.

Commenting on these findings David Geale said:

“Today’s research shows that fraud continues to evolve, and that reported fraud levels do not tell the whole story of fraud in the UK. It is important to take a whole system approach with social media platforms and other regulators to help tackle the problem at source. As we work ever more closely with the FCA, we are leveraging our combined powers and resources to tackle APP fraud at all levels.

“It is clear that more can be done to help victims know what they can do if they fall victim, and we expect firms to make sure everyone knows their rights.”

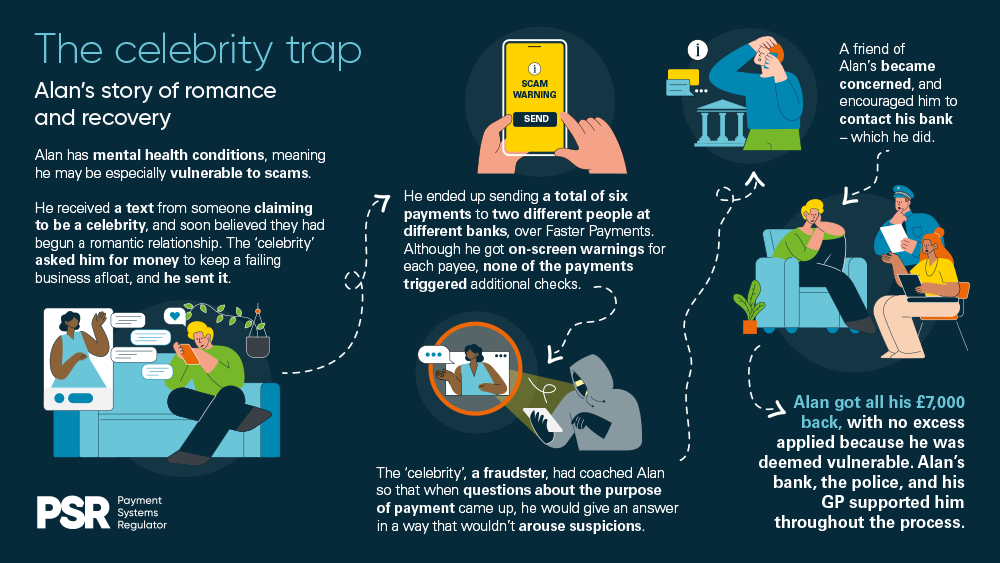

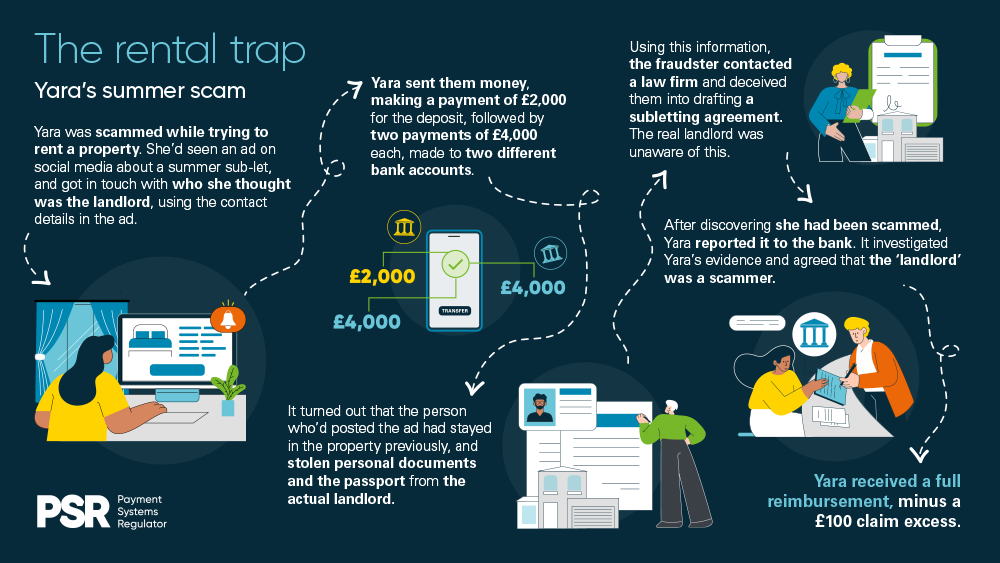

Behind every scam is a real person. The PSR has included some victim stories to highlight the various types of fraud via Faster Payments and what is in scope of our reimbursement policy. To keep victims anonymous, we have changed all identifiable characteristics in these case studies.

Case studies (click on the names to read the stories)

ENDS

Notes to editors:

The reimbursement rules apply to all qualifying APP transactions made via Faster Payments or CHAPS.

It’s not possible to make direct comparisons with data from before our policy due to methodology changes (particularly the definition of an APP scam). The latest figures only include APP scam claims that were reported to PSPs and were closed within the period covering 7 October 2024 to 30 June 2025.

The findings draw on a survey of 1448 UK adults, a nationally representative sample of 1012 UK adults and a boost of an additional 436 APP fraud victims since November 2024. 506 have fallen victim to APP fraud since November 2024.

The PSR has commissioned an independent review, which is being carried out by Frontier Economics, has begun, and we are expecting Frontier to conclude its work in the second quarter of 2026.

The PSR has today also published a blog post, ‘One year on: delivering fair outcomes through our APP scam reimbursement regime’, sharing practical insights for consumers and firms, based on what the PSR’s Supervision and Compliance Monitoring team have seen since the policy’s implementation in October 2024.