The ATM network is important to consumers and the economy. We know that consumers value the ability to access cash through a widely spread network of largely free-to-use (FTU) ATMs.

Our role is to ensure that the payment systems that facilitate consumers accessing cash are operated effectively and efficiently and in the interests of the evolving needs of service users.

Setting the scene

In 2016, cash was the most frequently used method of payment, representing 40% of all payments made in the UK. However, the proportion of cash payments is declining.

- This is the third consecutive year that cash represented less than 50% of payments made. This indicates that many consumers are turning to alternative payment methods.

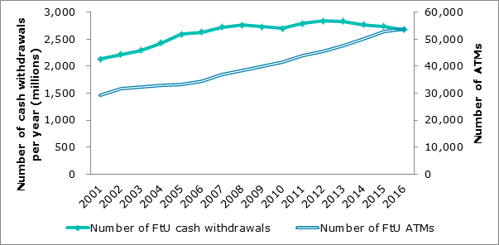

- The number of cash withdrawals from ATMs fell by around 10% between 2012 and 2017, from 2.8 to 2.5 billion.

- In 2016, 2.7 million consumers (5% of the UK adult population) relied almost entirely on cash.

- In June 2017, there were 70,308 ATMs in the UK.

- Of those, 78% were FTU and 22% were pay-to-use.

- Overwhelmingly, the majority of cash withdrawals are carried out at free to use ATMs (98%).

While the number of withdrawals has changed little over the last decade (with roughly the same number of withdrawals in 2016 as in 2006), the ATM estate has grown by more than 50%.

LINK is the UK’s main ATM network, which allows consumers to withdraw cash from ATMs which do not belong to their bank. Almost every ATM in the UK (both free and pay-to-use) is LINK enabled. All of the UK’s main debit and cash machine card issuers (predominantly banks and building societies) and the main cash machine operators (banks, building societies and independent ATM deployers) are members of LINK.

The Interchange Fee

Each time a consumer uses their debit card at a FTU ATM that does not belong to the banks that issued their card (issuing bank) a fee is paid by their bank to the ATM operator. This costs around 25pence per withdrawal and is called the interchange fee. This means consumers can use any ATM in the UK to access their cash or make transactions.

Alternatively, ATM operators may charge consumers to use their ATMs. In these cases, they cannot claim an interchange fee.

If a customer uses their own bank’s ATM, then no interchange fee will be charged.

Transactions carried out by consumers at their own banks are known as ‘on-us’ transactions.

A larger UK ATM estate and fewer ‘on-us’ transactions means banks are paying more in interchange fees. About £1 billion in interchange moves between LINK members annually. There has been a fall in on-us transactions, mainly due to the growth in the share of ATMs operated by independent ATM deployers (IADs) and a decline in the number of branch ATMs.

Financial Inclusion

LINK has a financial inclusion programme. This was designed and set up following work with the Treasury Select Committee under the chairmanship of John (now Lord) McFall in 2006. In addition, LINK has committed to protecting the geographic spread of ATM provision.

LINK’s financial inclusion programme works as follows:

- Subsidising the provision of FTU ATMs to ensure access to FTU ATMs in deprived areas.

- The subsidy is paid via a 10p interchange premium from LINK and available to deprived areas that do not have a free ATM within a kilometre from the nearest FTU ATM.

Over 1,500 priority areas across the country have benefited from new FTU ATMs as a result of this initiative.

As part of the development of interchange, LINK is exploring increasing the maximum amount of the subsidy to 30p to maintain extensive free access to cash for all in the UK.

LINK has announced that, regardless of any wider changes to interchange, it will protect the interchange fee for any FTU ATM that is currently one kilometre or more away from the next nearest FTU ATM.

What work has been taking place to ensure consumers can access their cash?

Our primary focus is to make sure that ATMs in the UK serve the needs of UK consumers. As well as closely monitoring the development of LINK’s proposals, we have been progressing a programme of work to inform how best the PSR can work to protect the interests of consumers.

We recently commissioned exploratory research which estimates that 75% of the UK’s adult population lives within one kilometre of a FTU cash machine. As mentioned above, LINK has recently announced that it will protect the interchange for any FTU ATM that is currently one kilometre or more away from the next nearest FTU ATM. This is a welcome development as it provides a level of protection for FTU ATM coverage and is consistent with the one kilometre distance guideline that has been used since the 2006 TSC review of ATMs.

Furthermore, following recent government investment the Post Office is committed to investing in their network and maintaining around 11,500 branches with no further substantive reductions and continued accessibility for all at the national level.

As a result of this initiative, 99% of the UK population will be within three miles of their nearest post office outlet and 90% of the UK population will be within one mile. This means that consumers will continue to be able to access cash using their local Post Office.

What happens next?

We set out three key requirements of LINK's proposals to ensure consumers continued to have widespread free access to cash. These were:

- a commitment by LINK to do whatever it takes to protect the current broad geographical spread of free-to-use (FTU) ATMs;

- that any cuts in interchange must be incremental and accompanied by close monitoring by LINK to understand the impact on the overall ATM estate – with action taken by LINK where the impact is not as expected; and

- for a greater focus on the Financial Inclusion programme – to continue to fill gaps in the FTU network.

While LINK’s announcement on its decision following its consultation has addressed these points, we will continue to actively monitor developments. The PSR will require LINK to report to it monthly on the impact of its decision and on the action that LINK has taken to address any unexpected negative impact on the FTU network. If any protected ATM is due to close, the PSR is keen to ensure there is a quick transition to a new operator without any adverse effects on consumers.

We will intervene if we believe the current broad geographical spread of free-to-use ATMs is threatened.

Find out more

Click the links below to learn more about the work we have been doing, along with copies of letters we have sent.

Hannah Nixon's letter to the Chair of the Treasury Select Committee

Hannah Nixon's letter to LINK, outlining our reporting requirements

-

The Scottish Free To Use ATM Network

pdf | 501.5 KB

-

ATM Impact Study Summary Findings

pdf | 267 KB

-

Exploratory Analysis Of The Prospects For, And Potential Impacts Of, ATM Scheme Competition

pdf | 116.4 KB

-

Our Quick Reference Guide To Our Monthly Reporting Requirements

pdf | 38.7 KB

-

Our Quick Reference Guide To Protecting Free To Use ATMs

pdf | 36.6 KB